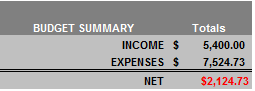

I’m a very organized person and keep all my statements in my file cabinet, so this exercise was easier than if I had none of the information at my fingertips. I went though the number five times to make sure they were correct.

So, once I picked myself up off the floor my first thought was, “how did I get here”? As I sat and looked at the numbers, I realized that this issue was masked by the fact that when my wife was there we had two incomes. Now that she was gone I had almost the same bills but only one income.

Here are some of the debts I was facing (numbers are rounded for ease of the blog).

- New Car – Loan $42,000 – Payment $708 – Worth $28,000 ($14,000 in the hole)

- Taxes Owed $10K – Payment $200 per month – Going up $245 per month with penalties and interest after paying $200 per month

- Credit Cards $15,000 – Payments $500 per month

There were many reasons why I got into the mess I was in; one of them being lack of money education. My parents and school never once talked about money, so when I was shipped off at 18 I was clueless. In my early years, I was in the music industry, which meant I was always broke. Since I grew up pampered in a middle class home, I used credit cards to supplement my non-existent income to maintain the life I was accustom to. I bought cars, music equipment, clothes, weekend getaways, dining out, renting more than I could afford, and on and on and on.

Over the years, from time to time, I would wake up and realize I had an issue and pay off the credit cards, but I would never change the way I thought or use money. So, it was not long before I was right back into the vicious cycle of using debt to live.

Four years ago, when I decided to get out of debt for the very last time in my life and made that spreadsheet, the three listed debts above were just the top three and that was only the tip of the iceberg. There was much more to the financial mess below the surface. After making the income and expense spread sheet that night four years ago, I turned off the lights and went back to bed, and although I had a lot of hard work ahead of myself, I felt liberated that I had a clear picture of where I was and what needed to be done. I had lived high on the hog and in denial for way too many years, and as Larry The Cable Guy always says it was time to “GIT-R-DONE”.

How Bad Is You Debt?

Do you have any idea what your financial picture is today? Are you still able to make the minimum monthly payment, or are you going under? Do you have any money left over to pay rent, utilities, or even buy groceries? Are you even able to answer these simple questions? Are you robbing Peter to pay Paul (Hah it is good to be me; everyone is always paying me after they steal from Peter), by transferring your balances in a false sense that you are making a dent in your debt? If this is where you are at the moment I feel for you and can empathize because I was in your shoes just a few short years ago. I’m sure you have heard the saying “misery loves company”, well rest assured you are not the only one in your situation. I bet the Joneses are in worse shape than you. Feel better yet? LOL

According to the 2024 American Household Credit Card Debt Study by Nerdwallet, the average U.S. Household with debt carries $15,355 in credit card debt and $129,579 in total debt. Here’s what the typical household is carrying, as well as total consumer debt in the U.S..:

|

|

Total owed by an average U.S. household with this debt

|

|

Percentage change for total owed between 2023 and 2024

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

How Can You Take Action Today

Here are a few things you can do now to get started in your quest for a new debt free way of life.

- Imagine yourself debt free and making wise financial choices.

- Wake up, like I did that faithful night, and stop living in denial. Acting like you don’t have a debt problem does not make it so. Check out my blog, Why Live In Debt: Denial

- STOP SHOPPING NOW!

- Fill out a monthly income and expense sheet and get a handle on what your financial picture is right now. CLICK HERE to Join our Budgeting Workshop and get hands-on with our easy-to-use spreadsheet! Learn how to create a budget, set up monthly cash flows, and take control of your money—step by step. Believe it or not, as painful as it is to see it in writing, it is also liberating to know where you stand.

- Sets some realistic financial and life goals

- Work with Paul Stryer as your personal financial coach and get one-on-one support, accountability, and guidance to take your financial journey to the next level. HIRE PAUL NOW!!!