Divorce is a challenging experience that impacts every facet of your life—especially your finances. While the process can feel overwhelming, it also presents an opportunity to forge a new path and take control of your financial future. With the right steps and guidance, you can rebuild your financial foundation and regain stability. I’m here to help you navigate this journey.

Let’s explore seven actionable steps to help you recover financially after divorce and reclaim your financial freedom.

Step 1: Take Stock of Your Financial Situation – Understand Your Starting Point

Before you can move forward, you need to understand exactly where you stand. The first step to financial recovery is to take a complete inventory of your financial picture. List all your assets (what you own), debts (what you owe), and income sources. Whether it’s the house, retirement accounts, investment portfolios, or credit card debt, knowing what you have and what you owe gives you a clear picture of your current financial reality.

How to get started: A simple spreadsheet can help organize this information. If you’re unsure where to start, free apps like Mint or EveryDollar can simplify the process by automatically tracking your accounts.

Why Live In Debt Spreadsheet: I find that a good old fashion spreadsheet is the most effective way to track your finances and progress. They are a little more manual but that is a good thing because you spend more time with your finances so you really get to know them, and feel the pain of where you have been, and the dopamine rush as you see your progress and wins before your very eyes. You can get the Financial Freedom Toolkit (spreadsheet) here: http://whyliveindebt.com/toolkit

Takeaway: Dedicate an hour this week to consolidating all your financial information into one document. This is the first step to clarity.

Linking Suggestion: Financial Freedom Toolkit (spreadsheet) here: http://whyliveindebt.com/toolkit

Step 2: Create a Post-Divorce Budget – Your Financial Roadmap

A budget isn’t about restriction; it’s about intention. It’s your financial GPS, guiding you through this new landscape. It helps you understand your new financial reality and plan accordingly. Start by listing your fixed expenses like rent, mortgage payments, insurance premiums, and utilities, then move to discretionary spending (the “fun stuff”).

Need help creating a budget? I’ve created a Google Sheet template http://whyliveindebt.com/toolkit that’s perfect for this. It helps you track your cash flow and shows you exactly where you can make adjustments to align your spending with your priorities.

Takeaway: Differentiate between your fixed and variable costs and prioritize the essentials. This helps you identify areas where you can potentially cut back.

Linking Suggestion: What to get a jumpstart on creating your budget, join the Why Live In Debt budgeting workshop and get step-by-step guidance on how to build, maintain, and live a budget, as well as gain a cheerleader that will cheer you on every step of the way. Join today: http://whyliveindebt.com/budgeting-workshop/

Step 3: Address Joint Debts and Financial Obligations – Untangling Your Finances

Ignoring joint debts can lead to significant financial setbacks down the road. It’s crucial to deal with them head-on. Contact your creditors proactively to separate accounts or transfer balances into individual names. This step ensures you’re no longer financially tied to your ex-spouse and protects your credit score.

A proven strategy: Many clients I work with successfully use the debt snowball method to eliminate debts one by one, starting with the smallest. This provides quick wins and builds momentum. We can use the same methodology to separate your finances, we just need to list them out and make a plan to contact your creditors, banks and other financial institutions. But we can do this one at a time and not take on the whole thing all at once.

Takeaway: Don’t delay. Make a plan to tackle your joint accounts systematically, starting today.

External Linking Suggestion: There is a great blog on the Kiplinger website that has some other great information on things not to forget. http://whyliveindebt.com/untangling-Finances

Step 4: Build a Financial Safety Net – Your Emergency Fund

Life’s unexpected challenges are easier to handle when you have a financial cushion. An emergency fund is your safety net, providing peace of mind and preventing you from going into debt when the unexpected happens. Start with a small, achievable goal of $1,000, then work toward saving three to six months of your essential living expenses.

Make it automatic: Automation can make this goal less intimidating. Set up automatic transfers from your checking account to a dedicated savings account every payday, even if it’s just a small amount like $25 per paycheck.

Rounding up: Another really cool way to add to your emergency fund is to use the round up method. When I use my chime debit card or Visa card the system rounds up to the nearest dollar and moves that amount from checking into savings. So lets say you spend $9.51 on your debit card, the system will move $.49 from checking into savings. Last year without even noticing i rounded up $2000+ into savings. I had forgot about it and when I looked at the end of the year I was shocked to see how much I had in savings.

Right now I am using chime as my debit card, visa card and savings. They have a round up program. They are also good at helping you build your credit back up if you credit score is low.

Use my refer code and sign up, and setup direct deposit to your chime checking account and we will both get $100 bucks deposited into our checking accounts. http://whyliveindebt.com/chime

How to enable round ups in chime:

- Go to Settings

- Tap Account Settings

- Scroll to Savings and tap Round up my purchases

- Toggle Round Ups on for debit and credit builder purchases

Takeaway: Open a separate, high-yield savings account specifically for your emergency fund and set up those automatic deposits.

External Linking Suggestion: Chime Referral: Use this link and join me with online banking with chime and get $100 free when you turn on direct deposit. http://whyliveindebt.com/chime

Step 5: Establish Long-Term Financial Goals – Envision Your Future

Now that you have a handle on your current finances, it’s time to look to the future. What does your ideal financial future look like? Are you saving for retirement, buying a house, paying off debt, or investing in your children’s education? Write down your long-term financial goals and break them down into actionable, smaller steps. This makes them feel less overwhelming and more achievable.

Let’s work together: As a financial coach, I guide clients through this very process. Together, we create personalized financial plans that align with their aspirations and set them on the path to success. Learn more about financial coaching: http://whyliveindebt.com/coaching/

Takeaway: Write down one SMART (Specific, Measurable, Achievable, Relevant, Time-bound) goal for your financial future today.

Internal Linking Suggestion: http://whyliveindebt.com/coaching/

Step 6: Seek Professional Guidance – You Don’t Have To Do This Alone

Recovering from a divorce is a journey, and you don’t have to go it alone. A financial coach can offer personalized strategies, support, and accountability, helping you navigate the complexities of your finances. As a Ramsey Certified Financial Coach, I specialize in helping people overcome financial challenges and achieve their financial dreams. I understand the emotional and financial toll divorce can take.

Takeaway: Schedule a free 30-minute consultation with me to explore how personalized financial coaching can help you rebuild your financial life.

Call to Action: Find a space on my consultation calendar: http://whyliveindebt.com/freeconsult

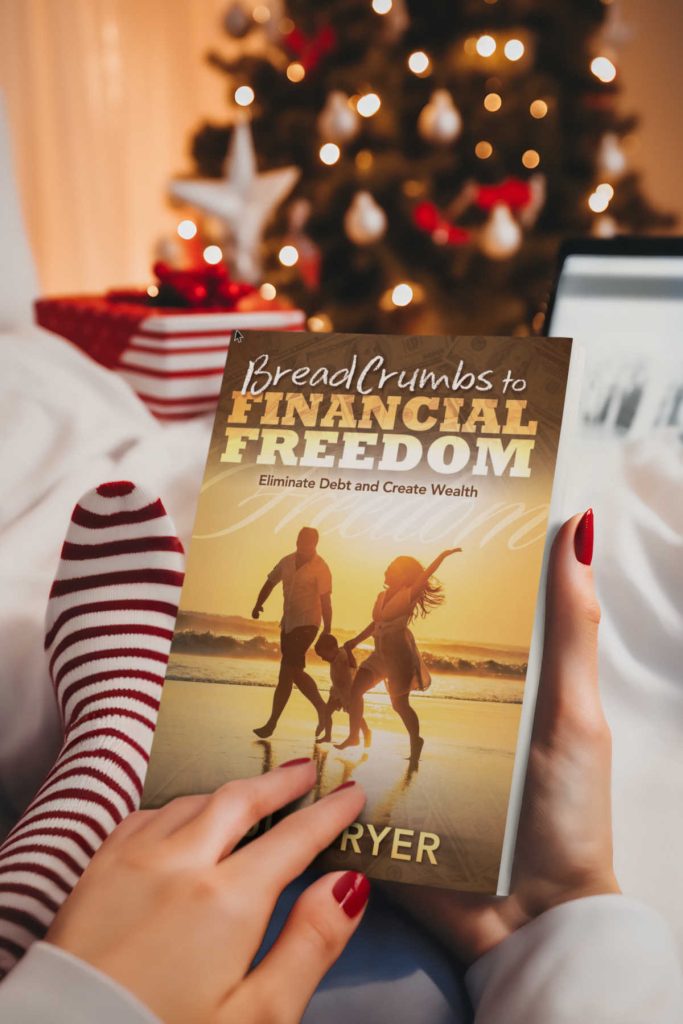

Step 7: Continue Your Financial Education – Knowledge is Power

The journey to financial freedom doesn’t stop here. Commit to continuous learning. Keep expanding your financial knowledge through books, podcasts, and workshops. My book, Breadcrumbs to Financial Freedom, provides a roadmap to financial success. It includes practical exercises and tools to help you stay on track and build a secure financial future.

Takeaway: Commit to learning one new financial concept each week. This will empower you to make informed decisions.

Linking Suggestion: Link “Breadcrumbs to Financial Freedom” to the book’s page on your website: http://whyliveindebt.com/breadcrumbs

External Linking Suggestion: Check out these few sites for more information.

Money Crashers: http://whyliveindebt.com/moneycrashers

Wise Bread: http://whyliveindebt.com/wisebread

Cleaver Girl Fiances: http://whyliveindebt.com/cleavergirl

Making Sense of Cents: http://whyliveindebt.com/cents

Afford Anything: http://whyliveindebt.com/affordanything

Money Saving Mom: http://whyliveindebt.com/moneysavingmom

Taking Control of Your Financial Future – Embrace Your New Beginning

Financial recovery after divorce takes time, but each step you take brings you closer to stability, independence, and peace of mind. By taking control of your finances, you’re laying the foundation for a brighter, more secure future.

Start today by scheduling your free consultation or grabbing a copy of my book, Breadcrumbs to Financial Freedom. Your next chapter begins now.