Smart Money Moves: FAQs for Debt Elimination

As I help people eliminate debt and build wealth, there are many questions that I get asked. But some of those questions get asked over and over again. In today’s blog I decided to put together a Frequently Asked Questions (FAQ) page, in the hopes it will help answer some of the more common questions.

Q: Should I borrow from my 401(k) or IRA to pay off debt?

A: This is a big mistake, and will be the most expensive money you ever remove from an account. The IRS calls this a Hardship withdrawal and has very tough restrictions on these types of withdrawals. You can also participate in a 401(k) loan that have to be paid back.

Hardship Withdrawal:

- Tax Penalties: Depending on your tax bracket you will be hit with a very high and expensive tax penalty, that could be as much as 25% or more of your withdrawal.

- Early Withdrawal Penalties: There is also a 10% early withdrawal penalty on top of the taxes owed.

- Contributions Stop: After a hardship withdrawal you are not allow to make contributions for six months. This means you could lose out on employer matching during this time.

401(k) Loan:

- If you get laid off or quit your job, the entire balance is due in full, usually within 60 days.

- If you can’t pay the balance the IRS considers this a distribution and the levy a 10% early withdrawal penalty.

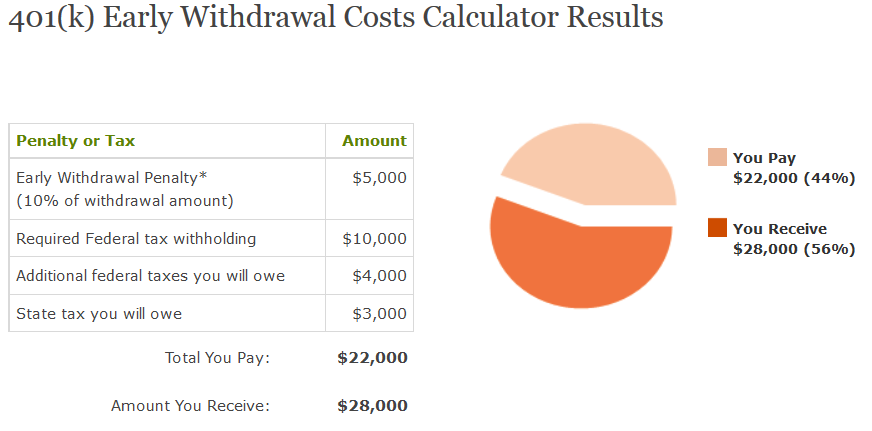

But as I said above this would be the most expensive money you ever withdrew. Here is an example of what it would cost to withdraw $50,000 from your 401(k), with a 28% federal tax bracket, and a 6% state income tax bracket.

For more information on Hardship Withdrawals and loans go to

https://www.irs.gov/retirement-plans/retirement-plans-faqs-regarding-hardship-distributions

Q: What is a rain-day fund?

A: A rainy-day fund sometimes called an emergency fund is a security blanket to help get through the unexpected events that will happen while you are living life. This could be for a home repair, car repair, unexpected medical bills, or even a job loss. This fund is not a Christmas gift fund, or vacation fund, it is solely for those unexpected emergencies that Mr. Murphy will send your way.

When following Breadcrumbs to Financial Freedom, in success step number one you will save up $1000 as a starter emergency fund. And as you work the 8 steps to financial freedom, in success step 3 you will build your rainy-day fund up to three to six months of expenses.

Q: Why should I pay off my smallest debt first, my bigger debts have higher interest?

A: In most cases when someone is in a bad financial situation, it is not something new to them. It is a learned behavior over time. Most people that are in dire straits and are hitting rock bottom are very emotion, and spend and make bad financial choices due to all the pain they are feeling. Funny thing is most people never change and will not permanently get out of debt until they have hit rock bottom. Most people will never change a behavior such as over spending until the pain of staying in debt is greater than the pain of changing.

Once a person makes a choice to change, they need encouragement to stay the course. People that go to AA have their meetings and their sponsor to help keep them stay accountable and encouraged. But in most cases people getting out of debt and changing a lifetime behavior don’t have a support group, but still require some kind of pat on the back to keep pushing forward.

That is where the “Debt Snowball” comes into play in step five of BreadCrumbs to Financial Freedom. If you pay the minimum on all your debt and go to town paying off your highest balance debt because it has a higher interest rate, it could take you a very long time to see a difference in the balance and pay it off. If you go to long without seeing results you will give up.

If you pay the minimum on all your debts and pay as much as you can to your smallest balance debt, it should hopefully be paid off pretty quick. The excitement of paying off that first debt will give you momentum to crush the 2nd smallest debt. It is all about seeing results and staying focused.

Q: How do I stay focused and stay on my budget?

A: Rule One, Make A Plan – Work The Plan. The eight success steps in Breadcrumbs to Financial Freedom is really a plan to eliminate debt and build wealth, and if you stick to the plan and work the plan you will see amazing results.

- Set some obtainable goals of things you would to accomplish in the near and distance future.

- Create a written budget. Most people try to keep everything about their finances in their head, and this only leads to one thing STRESS. It is a very liberating feeling to get all of your income and expenses down in writing, no matter if it is in a spreadsheet or on paper. Even if you use a spreadsheet I recommend you print it and put it up on the wall and look at it daily. Go to http://whyliveindebt.com/budgetcalc31 and down load our budget calculate in Microsoft Excel or printable PDF format, fill it in and get started on your new life today.

Check out my story to help inspire you to eliminate debt and build wealth.

http://whyliveindebt.com/mystory

Q: Should I stop putting money in my retirement, to pay off my debt?

A: There are a lot of experts out there that say yes you should stop putting any money into retirement, so you can use all the extra money towards paying off debt. And I agree to that for the most part (wait for it here comes the BUT clause). The one exception of when I disagree with all the other experts is when your company is matching your retirement contribution. If your company is matching you dollar for dollar up to X% of what you put into retirement, then I say lower your contributions down to the same level as what the company matches. So in this example set your contributions to 5%, if your company is matching you up to 5%. If you don’t take advantage of the matching contributions it is like throwing free money down the toilet.

- If your company does not match your contributions stop your contributions till your debt is paid off. Take all the extra funds and put them towards your debt.

- If your company does match your contributions, lower your contributions to the same level as what your companies maximum match amount.

Q: Should I take out a second loan on my home to pay off my debt?

A: You cannot rob Peter to pay Paul, or borrow your way out of debt. In most cases people that are in financial destress are looking for a quick fix, and think that consolidating all their debt onto a home loan or transferring the debt around on different credit cards is going to help them pay it off faster. When in fact in most cases this consolidation will actually cost you more and take longer to pay off.

The other factor here is the human factor. If you are that desperate that you are looking for a quick fix, you are not getting to the root of the problem. The issue is that you are dealing with bad habits that have been molded over years and years. You have to change the person inside as you work very hard to get out of debt. I have always told myself “The easy way is usually the wrong way” or in reverse “The hard way is usually the correct way”. I have found that when I’m at a cross roads in life, if I take the hard path I usually come out better then when I take the easy path.

The only real way to get out of debt is to “Make a Plan – and – Work the Plan”. In other words create a written budget, stay focused on the prize, pat yourself on the back for your wins, get extra jobs, and live on less than you earn.

Go to http://whyliveindebt.com/budgetcalc31 and down load our budget calculate in Google Sheets, fill it in and get started on your new life today.

I look forward to working with each and everyone one of you in the near future, and remember, each new day is another chance to change your life – you just have to find the right path and take action.

Check out this blog on the real cost of using credit cards

http://whyliveindebt.com/realcostofcreditcards

Latest Blogs

The Liberating Lie: How Embracing ‘Less’ Can Give You More

Y’all ever been drowning in bills, feeling like your paycheck got kidnapped before it even hit your account? It’s like […]

Read More

Transform Your Valentine’s Day with Lumi the Love Bot: Love Without Debt!

Try Lumi The Love Bot Now! Transform Your Valentine’s Day with Lumi the Love Bot: Love Without Debt! Valentine’s Day. […]

Read More

The Broke Romantic’s Valentine’s Survival Guide

Meet Lumi the Love Bot, your budget-savvy Cupid with a mission: “MAKE LOVE, NOT DEBT!” 💘 Lumi helps you craft […]

Read More

Breadcrumbs to Financial Freedom

Order your copy today and change your financial future forever. Order copies for all your friends and family this holiday season and give a gift that last a lifetime.

Breadcrumbs to Financial Freedom is your go-to guide for getting out of debt, building real wealth, and finally achieving financial independence. If you’ve ever felt stressed or stuck when it comes to managing your money, this book will walk you through simple, practical steps and help you shift your mindset so you can take control of your finances and turn things around. |

✅ Eliminate Debt: Learn proven strategies to pay off your debts and achieve financial freedom. |